أساسيات الصناديق الخاصة

فرص الاستثمار في الأسواق الخاصة نمَت بشكل كبير على مر السنين، مغرية المستثمرين المحتملين بعوائد قد تكون مربحة. ولكن في حين أثارت الأسواق الخاصة فضول المستثمرين، إلا أنها لا تزال فئة أصول غامضة.

إذا فكرت في الاستثمار في الأسواق الخاصة، فمن المحتمل أنك صادفت مفهوم الصناديق - وهي أدوات توفر العديد من المزايا للمستثمرين، مثل سهولة الوصول، والتنويع، والإدارة الاحترافية.

لكن تعلم تفاصيل الصناديق الخاصة قد يكون مربكًا - فأنت تواجه هياكل كيانات جديدة، ووثائق معاملات، ومصطلحات لم ترها من قبل.

سواء كنت تفكر في أول التزام لك بصندوق أو تسعى لتعميق معرفتك بالأسواق الخاصة، ستوضح لك هذه المقالة أساسيات كيفية عمل الصناديق وما يمكنك فعله للمشاركة.

ما هو الصندوق الخاص؟

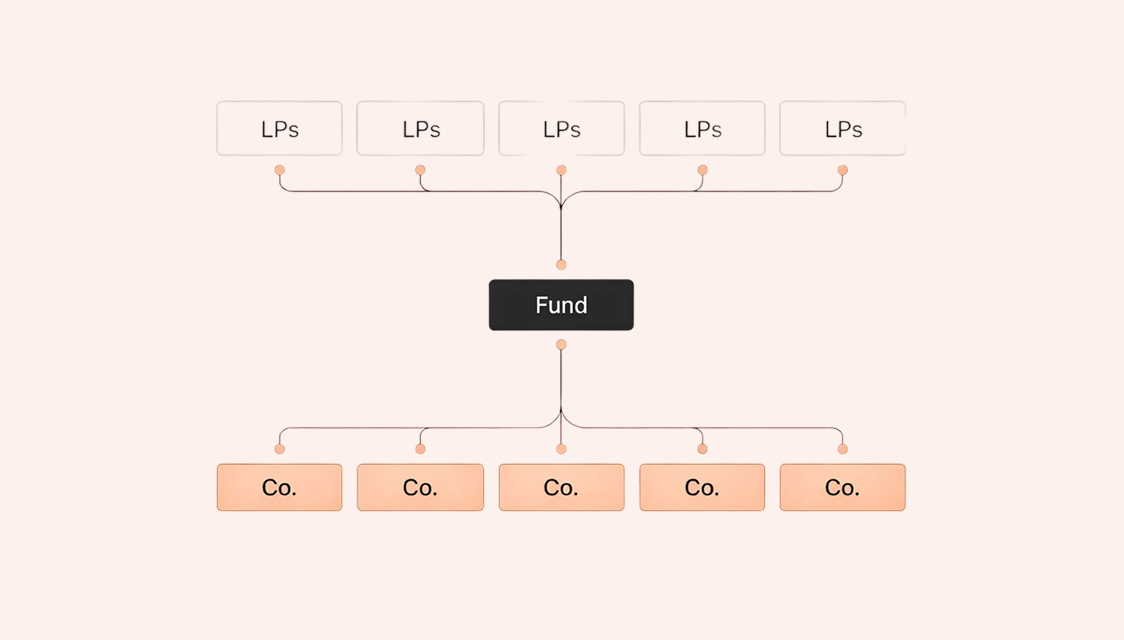

في جوهرها، الصناديق الخاصة هي تجمعات لرأس المال يتم جمعها من المستثمرين للاستثمار في أو شراء شركات خاصة (أي الشركات غير المتداولة في سوق الأوراق المالية). تُصنف هذه الصناديق عادةً على أنها صناديق رأس مال مخاطر، والتي تستثمر في الشركات الناشئة التكنولوجية عالية النمو، أو صناديق الأسهم الخاصة، التي تستثمر في أو تشتري شركات مستقرة ودائمة.

الصناديق الخاصة هي كيانات قانونية، تُنشأ عادةً كشراكة محدودة أو شركة ذات مسؤولية محدودة. داخل الصندوق، لديك مجموعتان أساسيتان من أصحاب المصلحة - الشركاء المحدودون (LPs) - وهم مستثمرون سلبيون، ولديهم مسؤولية قانونية محدودة، ويوفرون معظم رأس المال السهمي في الصندوق - والشركاء العامون (GPs) - المسؤولون عن البحث عن الصفقات، وإجراء العناية الواجبة، واتخاذ قرارات الاستثمار، وفي النهاية التخارج من تلك الاستثمارات.

هذه العلاقة بين الشركاء المحدودين والشركاء العامين هي العمود الفقري لكل صندوق خاص، سواء في رأس المال المخاطر أو الأسهم الخاصة.

فهم العلاقة بين الشريك العام والشريك المحدود

تم تصميم العلاقة بين الشركاء العامين والمحدودين لمواءمة الحوافز الاقتصادية وتحكمها اتفاقية قانونية تسمى اتفاقية الشراكة المحدودة (LPA). تحدد هذه الوثيقة كل شيء: مقدار ما يتقاضاه الشريك العام، وكيفية تقسيم العوائد، وما هي حقوق الشركاء المحدودين، وماذا يحدث إذا ساءت الأمور.

يحصل الشريك العام على نوعين من التعويضات: رسوم الإدارة والفائدة المحمولة.

تتراوح رسوم الإدارة عادةً بين 1.5% و 2.5% من رأس المال الملتزم به، وتُدفع سنويًا لتغطية التكاليف التشغيلية. فكر في الرواتب، وإيجار المكاتب، ومصاريف العناية الواجبة—كل ما هو مطلوب لإدارة شركة استثمار احترافية.

إليك مثال على شكل هذا البند في اتفاقية الشراكة المحدودة (LPA).

ثم هناك "الكاري" (carry)، وهو اختصار لـ "الفائدة المحمولة" (carried interest). هذا هو نصيب الشريك العام من الأرباح، وغالبًا ما يكون 20%، ولكن فقط بعد أن يسترد الشركاء المحدودون أموالهم بالإضافة إلى عائد أدنى (عادة حوالي 8%). يُطلق على هذا الحد الأدنى اسم العائد المفضل أو معدل العتبة، وهو شائع بين الصناديق الخاصة لضمان حصول المستثمرين على عائد أدنى محدد مسبقًا ولمواءمة الحوافز الاقتصادية بين الشريك العام والشركاء المحدودين في الصندوق.

الترتيب الذي يتم به تقسيم التوزيعات بين الشركاء المحدودين (LPs) والشركاء العامين (GPs) يُشار إليه باسم "الشلال"، والذي سنتناوله بمزيد من التفصيل أدناه.

يمنح هذا الترتيب الشريك العام (GP) دافعًا قويًا لتحقيق عوائد. إذا كان أداء الصندوق جيدًا، فإنهم يشاركون في الأرباح، ولكن فقط بعد أن يحصل الشركاء المحدودون (LPs) على العائد المفضل الذي يحق لهم. إذا لم يكن أداء الصندوق جيدًا، فإن الشركاء العامين (GPs) لا يزالون يحصلون على رسوم إدارتهم لتغطية مصاريف الصندوق ورواتب الموظفين، لكنهم لن يحصلوا على أي مكافآت أداء.

دورة رأس مال الصندوق الخاص

عندما يلتزم مستثمر بصندوق، فإنه لا يحول المبلغ بالكامل في اليوم الأول. بدلاً من ذلك، يصدر الشريك العام (GP) طلبات رأس المال حسب الحاجة، والتي غالبًا ما تحدث خلال السنوات القليلة الأولى من عمر الصندوق. يمنح هذا النهج التمويلي المرحلي الشريك العام (GP) مرونة ويسمح للشركاء المحدودين (LPs) بإبقاء رأس المال غير المستخدم مستثمرًا في مكان آخر في هذه الأثناء.

هذا ما يمكن أن يبدو عليه بند طلب رأس المال في اتفاقية الشراكة المحدودة (LPA).

بمجرد إتمام الاستثمارات، تتمثل مهمة الشريك العام (GP) في مساعدة الشركات التابعة للمحفظة على زيادة قيمتها—من خلال التحسينات التشغيلية، وعمليات الاستحواذ الإضافية، وتطوير المواهب، أو التموضع الاستراتيجي. بمرور الوقت، يبدأ الشريك العام (GP) في بيع تلك المراكز (التي تسمى مخارج) وإعادة النقد إلى الشركاء المحدودين (LPs).

يتم تحديد توقيت هذه التدفقات النقدية في هيكل يُعرف باسم الشلال. وهو يحدد من يحصل على الدفع، وبأي ترتيب. في معظم الحالات، يسترد الشركاء المحدودون (LPs) رأس مالهم الأصلي، بالإضافة إلى العائد المفضل، قبل أن يحصل الشريك العام (GP) على أي حصة من الأرباح.

تقوم بعض الصناديق بتقسيم الأرباح على أساس كل صفقة على حدة (يُسمى "الشلال الأمريكي")، بينما تقوم صناديق أخرى بتنظيم توزيعات أرباحها بناءً على أنشطة الصندوق بأكمله (يُشار إليه باسم "الشلال الأوروبي"). في الحالة الأوروبية، لا يحصل الشريك العام (GP) على حصة من الأرباح حتى يحقق الصندوق بأكمله العائد المفضل. يفضل معظم المستثمرين المؤسسيين هذا الأخير (فهو أكثر تحفظًا ويجعل الجميع متوافقين على المدى الطويل).

ماذا يحدث خلال عمر الصندوق

بينما تُعتبر بعض الصناديق الخاصة "دائمة"، مما يعني أنها صناديق مفتوحة لا يوجد لها تاريخ انتهاء محدد، فإن معظم الصناديق الخاصة ليست دائمة. غالبًا ما يكون لها عمر محدد - عادة حوالي 10 سنوات - وستمنح تمديدات في بعض الأحيان.

تُعرف السنوات القليلة الأولى بفترة الاستثمار، حيث يقوم الشريك العام (GP) بجمع ونشر رأس المال بنشاط في صفقات جديدة. بعد ذلك، يتحول التركيز إلى خلق القيمة والمخارج. تميل العوائد إلى الظهور في وقت لاحق من عمر الصندوق، وهذا هو السبب في اعتبار الأسهم الخاصة فئة أصول غير سائلة وطويلة الأجل.

الجدول الزمني العام يبدو كالتالي:

- السنوات 0-3: جمع الأموال، طلبات رأس المال، الاستثمارات المبكرة

- السنوات 4-6: خلق القيمة؛ تنمو محفظة الصندوق مع توسع الشركات

- السنوات 7-10: المخارج، التوزيعات، وتصفية الصندوق

بما أن الأموال تُطلب وتُعاد على مراحل، فمن الشائع أن يعيد المستثمرون استثمارها في صناديق جديدة بمرور الوقت للحفاظ على تعرضهم للسوق. لهذا السبب، غالبًا ما يلتزم المستثمرون المحدودون (LPs) ذوو الخبرة بالعديد من الصناديق المتتالية (أي الصناديق التي تبدأ في سنوات لاحقة) من نفس المدير.

نصائح العناية الواجبة للمستثمرين المحدودين (LPs)

ليست كل الصناديق متساوية. إذا كنت تفكر في الاستثمار في صندوق خاص، فهناك بعض الأمور التي يجب البحث عنها أبعد من توقعات الأداء.

- سجل الأداء: هل حقق الشريك العام (GP) عوائد حقيقية ومحققة؟

- وضوح الاستراتيجية: هل لدى الشريك العام (GP) خطة عمل واضحة وقابلة للتكرار؟

- مشاركة شخصية: ما مقدار رأس مال الصندوق الذي يلتزم به الشريك العام (GP) شخصيًا؟

- التوافق: هل تضمن شروط الصندوق أن يحقق الشريك العام (GP) الربح عندما يحقق المستثمرون المحدودون (LPs) الربح، وليس قبل ذلك؟

- الشفافية: هل سيشارك الشريك العام (GP) تحديثات منتظمة، وبيانات مالية مدققة، وإفصاحًا كاملاً عن الرسوم؟

انظر أيضًا إلى شروط الحوكمة في اتفاقية الشراكة المحدودة (LPA) - أمور مثل بند الشخص الرئيسي (الذي يوقف الاستثمار إذا غادر عضو فريق معين) أو بند "الطلاق بلا خطأ" (الذي يمنح المستثمرين المحدودين (LPs) صلاحية عزل الشريك العام (GP) في ظل ظروف معينة). لا تُناقش هذه الأمور كثيرًا في مواد جمع التبرعات، لكنها قد تتحقق في الواقع.

كيف يمكن لـ Zest أن يساعد

تعمل Zest على رقمنة معاملات السوق الخاص، وتبني أدوات لتبسيط كيفية تعامل رواد الأعمال والصناديق والمستثمرين. تم تصميم منصتنا لتوفير وقتك وتقليل التكاليف الإدارية، مما يبسط عملية المعاملات من البداية إلى النهاية.

Subscribe to the Zest Wire. Insights on private markets.

Biweekly practitioner insights on capital activity, market trends, and conversations shaping MENA and emerging private markets.

From our blog

منصة الأسواق الخاصة التي يطالب بها صانعو الصفقات اليوم.