Continuation funds: the GP’s new exit playbook

The exit window in private markets has been tight for years, and LPs in the GCC are growing increasingly vocal about one thing: they want their money back.

Enter the continuation fund.

Once associated with distressed assets and zombie funds, continuation vehicles have undergone a makeover. Today, they are among the fastest-growing tools in private markets, used by GPs to hold onto their best-performing assets while providing liquidity to LPs who need it. And they are no longer just a private equity tool. Investors across all types of private assets are now adopting them.

Here is what you need to know.

What is a continuation fund?

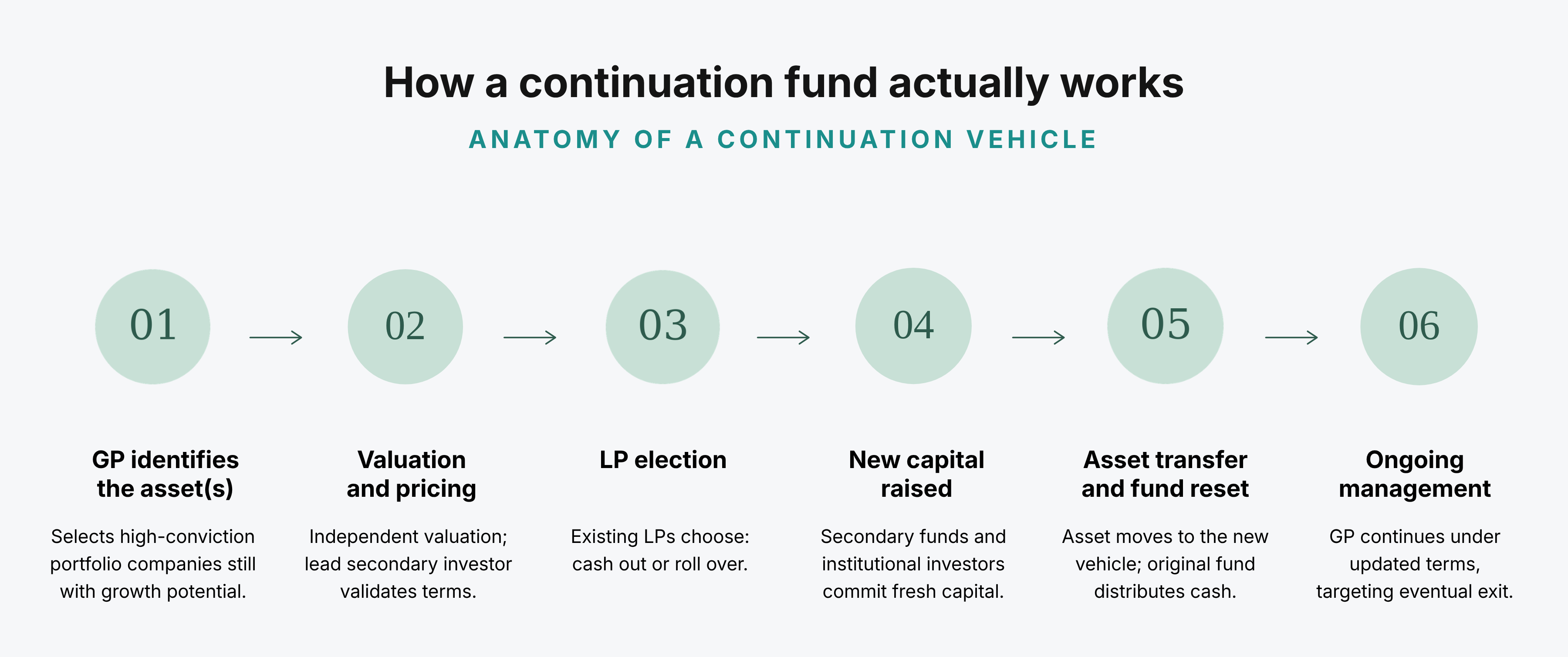

A continuation fund is a new investment vehicle created by a GP to acquire one or more assets from an existing, aging fund.

Most private market funds operate on a fixed term, typically 10 years, after which the GP is contractually required to wind down the vehicle, exit remaining positions, and return capital to LPs. As that 10-year timeline approaches, GPs must decide whether to sell the remaining assets or extend their ownership.

The continuation fund acts as a reset button: the GP moves its best assets (the ones that they believe still have room to grow) into a new vehicle with fresh capital, fresh terms, and a new clock.

The key benefit to LPs is choice. When a continuation fund is formed, existing LPs in the original fund are typically given two options:

- Cash out: Sell their interest and receive liquidity at a price set during the transaction.

- Roll over: Transfer their interest into the new continuation vehicle and maintain their exposure to the asset(s).

Where does the cash come from? Dedicated secondary funds and institutional investors step in, buying out the LPs who want liquidity and funding the vehicle going forward. The GP retains management of the asset(s), typically with a refreshed fee structure, and continues pursuing the value creation plan.

Continuation funds can hold a single asset or a basket of portfolio companies. Single-asset vehicles have become more popular, accounting for the majority of continuation fund volume, as GPs increasingly use them to extend the life of their highest-conviction assets.

Why continuation funds are booming

Secondary transactions across the world hit a record $226 billion in 2025, up 41% from the prior year, while GP-led secondaries (driven by continuation funds) reached $106 billion in 2025, nearly 50% higher than the previous year.

Several forces are driving the acceleration:

The exit bottleneck

Traditional exit routes, such as IPOs and M&A transactions, have not kept pace with the volume of capital deployed in private markets over the last decade. Global buyout funds hold an estimated 29,000 unsold portfolio companies worth an estimated $3.6 trillion. At the current pace of exits, it would take nearly 20 years to work through that backlog. GPs need alternatives, and continuation funds offer one.

LP demand for liquidity

LPs have been patient, but their patience may be wearing thin. After years of declining distributions, investors are actively seeking liquidity options. While private market investors plan to increase their private equity allocations, they expect to have liquidity opportunities in the future.

Continuation funds give GPs a way to return cash to LPs who need it while allowing other LPs to continue holding the asset. Since distributions are the metric LPs increasingly weigh when deciding whether to commit to a manager's next fund, a GP who delivers DPI (distributions to paid-in capital) through a continuation vehicle strengthens the relationship for future vintages.

GPs do not want to sell their winners

This is a primary reason why GPs are pursuing continuation funds today.

In this scenario, a fund may be approaching the end of its term, but the GP has a portfolio company that is performing well and has not yet reached its full potential. Selling now would leave money on the table, but the fund’s Limited Partnership Agreement (LPA) requires the GP to wind down the fund. Even in scenarios where the GP wants to sell certain portfolio companies, the timing and terms are not always right.

A continuation vehicle allows the GP to hold onto the asset, continue executing their strategy, and avoid a fire sale at a steep discount.

Venture capital is catching up

Continuation funds were originally a PE tool, but VC firms are now embracing them as exit timelines extend and the median time to exit for VC-backed companies stretches toward nine years.

Examples include Lightspeed Venture Partners raising a $1 billion continuation fund, while other firms like General Catalyst, New Enterprise Associates, and Insight Partners have explored or launched similar vehicles. For VC firms holding onto high-growth companies, continuation funds offer a path to liquidity that does not depend on going public.

How a continuation fund actually works

Single-asset vs. multi-asset continuation funds

Continuation funds come in one of two types: single-asset or multi-asset.

Single-asset continuation funds hold one portfolio company and have become the most popular structure in recent years. LPs often prefer single-asset continuation funds because they can underwrite a single company and assess the risk and reward without the added complexity of multiple assets. Single-asset vehicles are structurally similar to SPVs in their simplicity and ease of maintenance.

On the other hand, multi-asset continuation funds hold a basket of companies, typically the strongest remaining positions from an aging fund. These give GPs more flexibility, but they can make it harder for LPs to decide whether to continue their exposure to the underlying companies. LPs are underwriting multiple theses at once, and the quality of the basket can vary. For LPs with strong views on specific companies in the portfolio, this mixed basket can be a drawback.

The trend toward single-asset vehicles reflects what both sides of the table want right now. GPs get to double down on their highest-conviction winners, and secondary buyers get to underwrite a single, well-defined thesis rather than a blended basket.

Key considerations for GPs and LPs

Continuation funds have several benefits, but they can be complex to execute. Here is what both sides of the table should keep in mind.

For GPs

- Conflicts of interest are the primary concern. The GP is both the seller (from the original fund) and the buyer (into the continuation vehicle). Transparent valuation, independent pricing, and LPAC involvement are essential to maintaining trust.

- GP commitment matters. Nearly 90% of continuation fund deals in 2024 involved GPs rolling 100% of their available proceeds into the new vehicle. Skin in the game signals conviction and aligns interests.

- Execution is resource-intensive. Continuation vehicles require coordination across LPs, portfolio companies, secondary buyers, legal counsel, and advisors. They can take several quarters to close, so it’s important for GPs to start planning the transition early on, rather than leaving it to the last few months before the fund’s deadline.

For LPs

- Understand the election carefully. Cashing out provides immediate liquidity but means forgoing future upside. Rolling over means continuing your exposure, but under refreshed terms that may include new fees and carry structures.

- Look at the composition of the vehicle. If the continuation fund holds multiple assets, there are factors to consider. Are these all high-conviction winners the GP wants to double down on, or is the basket padded with some average-performing positions the GP is having trouble selling? The composition of the fund can uncover the GP's actual motivation for the transaction.

- Analyze the fee structure. Continuation vehicles often come with refreshed management fees and carry terms that can vary widely from the original fund. Some deals let the GP collect the carry they have earned on the asset to date and then reset the carry clock under the new vehicle's terms; others stack fees in ways that meaningfully change the economics for continuing LPs. Compare the proposed terms against what you would expect from a primary commitment to the GP.

- Check the valuation. The transaction price determines what cashing-out LPs receive. Ensure independent validation has been conducted and that the pricing reflects current market conditions.

- Evaluate the GP’s track record with the asset. A continuation fund is ultimately a bet on the GP to continue creating value. Ask why the asset has not been exited yet, what the future plan looks like, and determine whether the GP has earned your trust.

Why this matters in MENA

The MENA region is likely to become the next hub for GP-led secondary volume.

The region’s private markets are maturing rapidly. MENA's private markets are growing quickly, with investment and M&A activity surging year-over-year (for a deeper look at the data, see our 2026 outlook). As fund vintages start to age, GPs in the region will increasingly face the same liquidity pressures that drove PE and VC firms in other regions to pursue continuation vehicles.

Regional exit pathways are expanding but selective. IPO activity has grown across the GCC, but listings remain selective, and the pipeline cannot absorb every GP’s portfolio. For fund managers, continuation funds offer a third option between selling too early and holding on too long.

LPs in the region are sophisticated and liquidity-aware. Family offices, sovereign wealth funds, and institutional investors in the region are increasingly familiar with secondary market mechanics. Continuation vehicles align well with their need for flexibility to take liquidity when they need it, or stay invested when they believe in the upside.

The market trends that powered the GP-led secondary boom in other regional markets are now converging in MENA. As funds continue to age and exit windows stay narrow, continuation vehicles are likely to move from a niche PE tool to mainstream across the region's private markets.

How Zest can help

Zest is a digital transactional infrastructure company powering private-market transactions. Zest offers a layer of digital execution capabilities for SPV formation and deal workflow management, as well as FSRA-regulated escrow and arranging services, that together simplify, safeguard, and scale private-market transactions on one digital platform.